What can private investors expect from the markets in the medium term? The experts in the Swiss Life Group address this question every June. Our scenarios for the next three years show which forces are likely to shape the markets in the medium term: in the baseline scenario, we expect further growth, supported by significant investments in infrastructure, sustainable energy, defence and artificial intelligence. Companies have demonstrated their resilience and are using the environment to further increase their profits. This means that investments in real assets will continue to be favoured over bonds.

The most important facts at a glance

Every year in June, the Swiss Life Group develops its medium-term scenarios for the next three years. They serve as a strategic compass for the portfolio focus and help in assessing economic and financial developments. They also offer private investors guidance in a constantly challenging market environment and encourage them to take a long-term view of investment decisions instead of focusing on short-term fluctuations.

In the baseline scenario, economic growth is supported by significant investments in infrastructure, sustainable energy, defence and artificial intelligence. At the same time, companies benefit from stronger balance sheets and increased adaptability, which enables further earnings growth.

In this scenario, we expect inflation to peak in the second half of 2026 and decline thereafter. This will give the central banks scope to ease monetary policy moderately from 2027. All in all, a constructive environment is thus emerging for the financial markets.

The first alternative scenario describes a global recession triggered by a demand or supply shock, with varying impacts on inflation and asset classes.

The second alternative scenario outlines an above-average upswing, supported by faster falling energy prices or stronger productivity gains. Growth is accelerating without a sharp rise in inflation in the short term, benefiting almost all asset classes.

Swiss Life’s Chief Economist Marc Alain Brütsch explains the economic scenarios in the video. You can read our expert assessment below.

Half-year review 2026: where do we stand?

Those who had hoped for a calmer period following an eventful 2025 were clearly surprised in the first half of 2026. Global developments were dominated by three themes. The US played a key role in all of them.

1. Geopolitical conflicts

The first quarter of 2026 was dominated by geopolitical developments:

- The US caused international uproar in January with the arrest of Venezuelan President Nicolás Maduro, which gave it direct access to the largest known oil reserves.

- Shortly thereafter, tensions with its European NATO partners escalated when the US administration laid a claim to Greenland for security reasons.

- A further escalation followed on 28 February with the US and Israeli military attack on Iran. The subsequent blockade of the Strait of Hormuz led to the biggest disruption to the global oil market in history, pushing up energy prices across the world.

In the meantime, there are signs of easing: by signing a Memorandum of Understanding on 17 June, the US and Iran have taken an important step towards de-escalation. The reopening of the Strait of Hormuz removes a major burden for the global economy. However, long-term stability has yet to be established, in particular with regard to regulating Iran’s nuclear programme. However, a comprehensive peace agreement is to be formulated over the next 60 days.

At the same time, the dynamics of the war in Ukraine have changed. Progress in Ukraine’s drone warfare has slowed Russia’s territorial gains, significantly increased the costs of war and casualties for Russia, and carried the war far into Russia. This could increase Russia’s willingness to engage in serious negotiations over the medium term.

2. Artificial intelligence (AI)

Momentum in the field of artificial intelligence continues. The main focus is on hugely expanding computing capacities: the five big US technology companies Amazon, Alphabet (Google), Meta, Microsoft and Oracle could increase their investments in AI infrastructure to up to USD 800 billion in 2026 – an increase of over 70% compared to the previous year. Analysts at the investment bank Morgan Stanley estimate that the investments of these five companies alone could increase to up to USD 1100 billion in 2027, which would be roughly equivalent to Switzerland’s annual gross domestic product.

The semiconductor industry in particular is benefitting from this, as high-performance chips account for a large proportion of investments. As a result, sales, profits and valuations of leading chip manufacturers increased sharply.

In terms of technology, the introduction of so-called AI agents attracted attention in February. These systems can independently plan and execute complex tasks, potentially challenging the traditional software-as-a-service model. At the same time, discussions about the implications of artificial intelligence for society, especially in terms of employment, increased significantly.

The regulatory situation intensified in June: the US Department of Commerce ordered the AI startup Anthropic to block foreign users from accessing its most advanced AI model. For the first time, export bans were imposed not only on advanced semiconductor technology, but also on an AI model itself, which in turn underscores the strategic importance of AI and fuels global aspirations for technological superiority.

3. US trade conflict

In the trade conflict, the US Supreme Court ruled on 20 February that the tariffs imposed on the basis of the International Emergency Economic Powers Act (IEEPA) were illegal and had to be withdrawn.

The US government reacted immediately with temporary tariffs of 10% for a maximum duration of 150 days. At the same time, it commissioned the US Trade Representative to investigate possible trade disadvantages experienced by the US, which provide justification for permanent tariffs under Section 301 of the US Trade Act.

Meanwhile, the US Trade Representative has proposed tariffs ranging from 10 to 12.5% against a total of 60 countries, including Switzerland and the EU. The reason for this is that these countries either do not have a ban on imports of goods produced under forced labour or, from the point of view of the United States, they do not sufficiently enforce such laws.

Currently, there are strong indications of a more orderly and predictable US trade policy. Nevertheless, key trading partners will have to prepare for additional import tariffs of at least 10% over the long term. The pressure to conclude bilateral agreements to gain greater planning security remains correspondingly high.

Financial markets amid the tension between the Iran war, tighter monetary policy and rising corporate profits

Rising inflation burdened bond markets

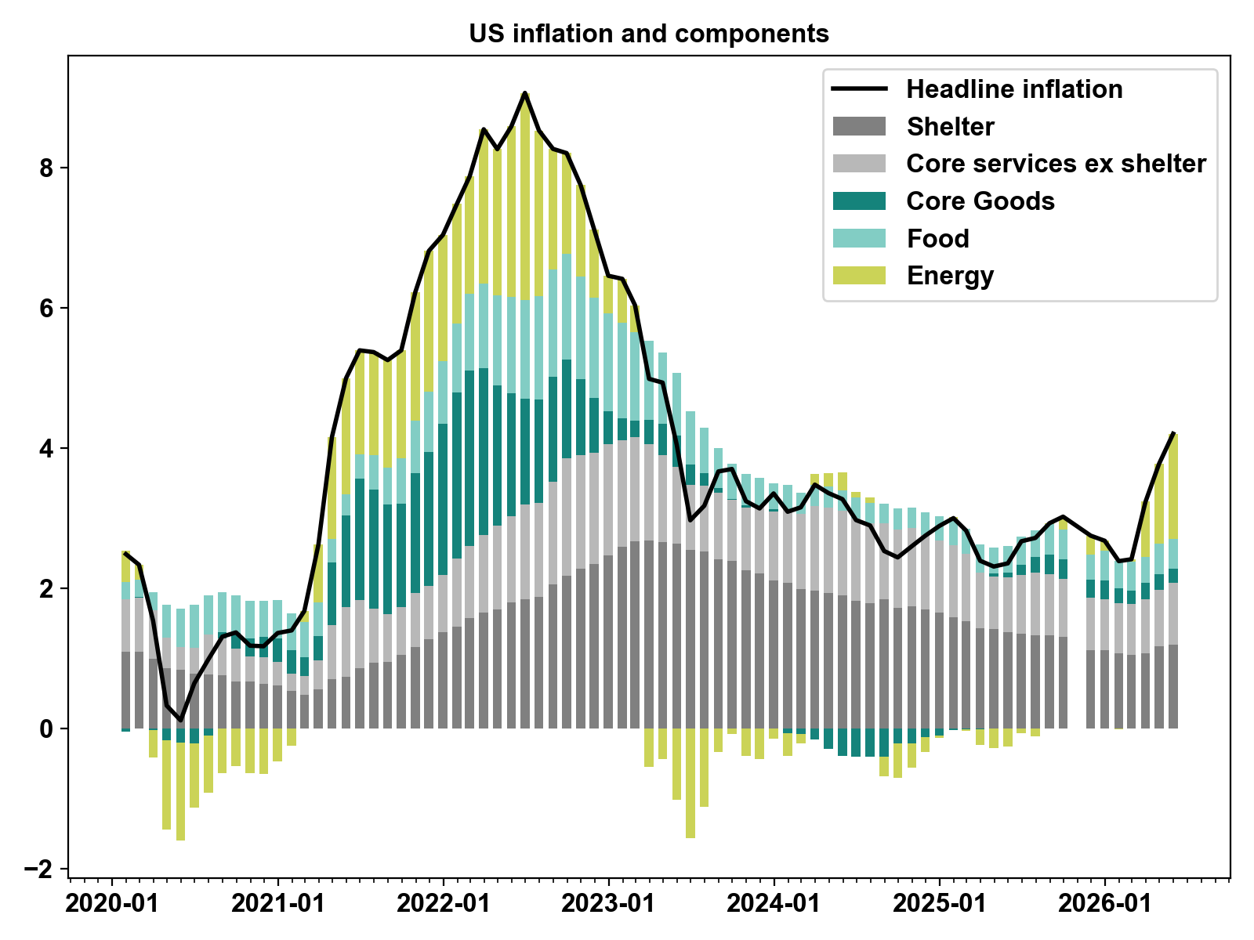

The significant rise in energy prices in the wake of the Iran conflict pushed global inflation up noticeably. In the US, headline inflation reached 4.2% in May, ending the previously observed decline (see figure 1).

Figure 1: The rise in oil prices put an end to the downward trend in US inflation and caused it to rise to 4.2% in May. Source: Bloomberg, Swiss Life Wealth Managers.

The surge in inflation put increased pressure on central banks to take action. The European Central Bank raised the key interest rate to 2.25% in June; a further hike to 2.5% by the end of the year is considered likely. Expectations have also shifted significantly in the US: instead of the interest rate cuts priced in at the start of the year, the focus is now even shifting to a potential interest rate hike.

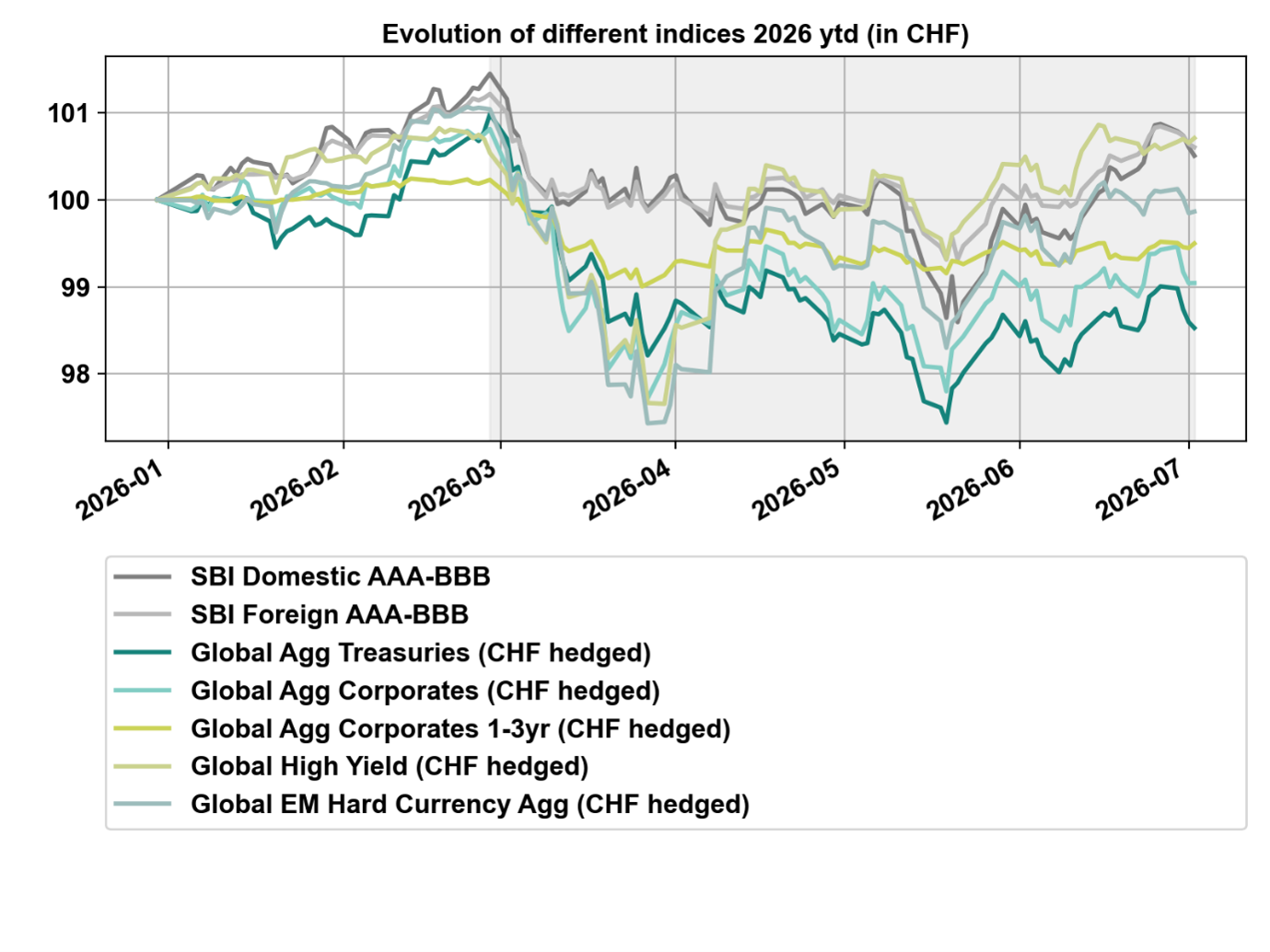

This revaluation of monetary policy led to rising risk-free interest rates globally and weighed correspondingly on bond prices. After a solid start to the year, government bonds in particular came under pressure. Markets have not fully recovered from these losses so far and remain volatile (see figure 2).

Figure 2: After a good start to 2026, expectations of tighter monetary policy in response to the Iran war caused interest rates to rise globally. Rising interest rates caused bond prices to fall, especially government bonds. Bond markets have not yet recovered from the losses and remained volatile. (Data up to 02.07.2026. The period of the Iran War is shaded in grey.) Source: Bloomberg, Swiss Life Wealth Managers.

Equity markets proved resilient

Equity markets also had a strong start to 2026, before the Iran conflict led to a correction in March. However, in view of the significant upheavals on the energy market, this was comparatively moderate. The expectation quickly gained ground that the conflict would remain temporary and not trigger a sustained trend reversal.

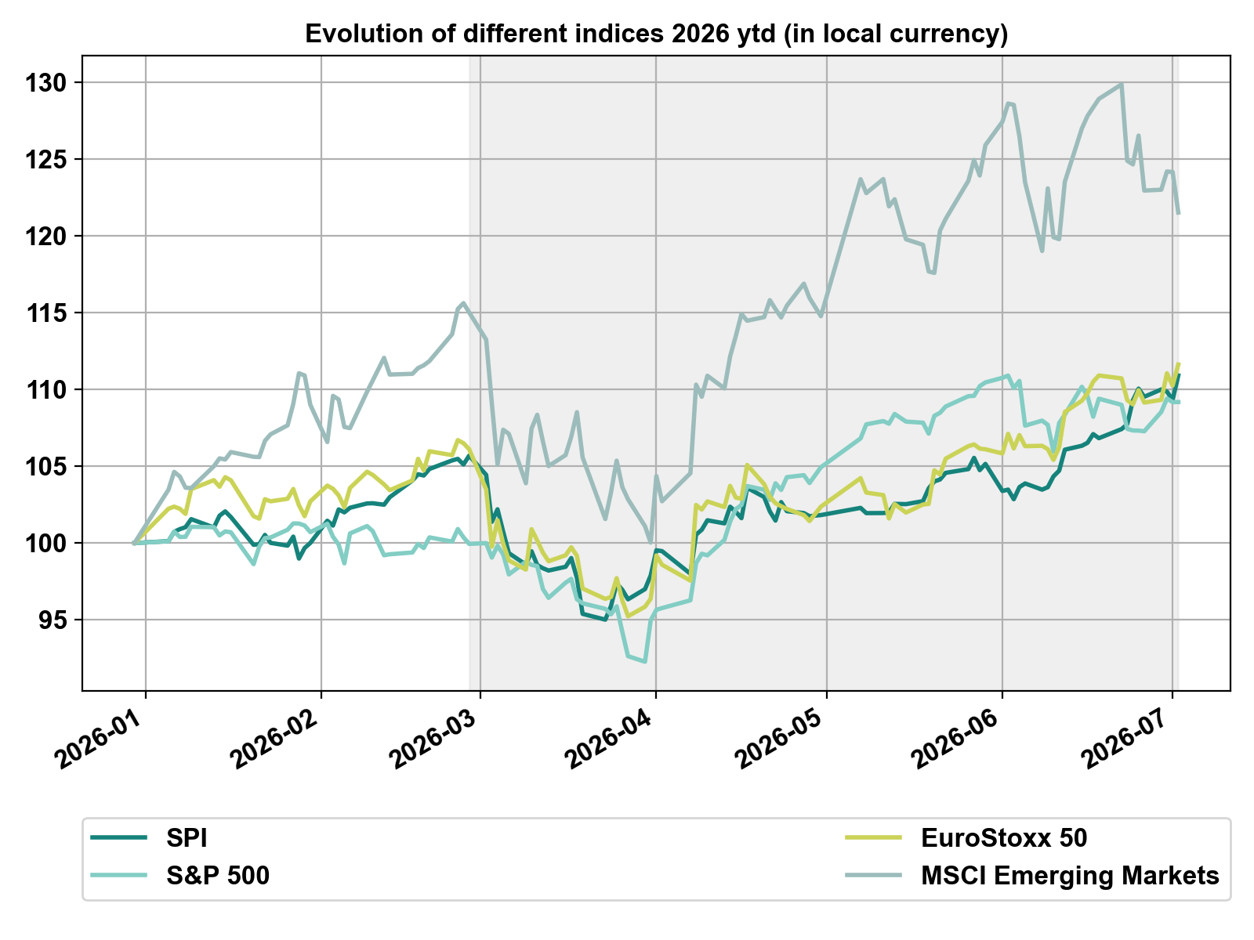

Since April, equity markets have experienced a strong recovery (see figure 3). This was supported by the prospect of an easing of the situation in the Middle East and by surprisingly strong corporate earnings in the first quarter.

Figure 3: After a good start to the year and a correction in March, equity markets have rallied impressively since April, fuelled both by expectations of an imminent end to the war in the Persian Gulf and by surprisingly good corporate earnings. (Data up to 02.07.2026. The period of the Iran War is shaded in grey.) Source: Bloomberg, Swiss Life Wealth Managers

The increasing breadth of the market is noteworthy: earnings growth is no longer confined to the big US tech companies. Other sectors are also benefiting from increased investment in infrastructure, energy, mobility and defence.

Equities remained the leading asset class

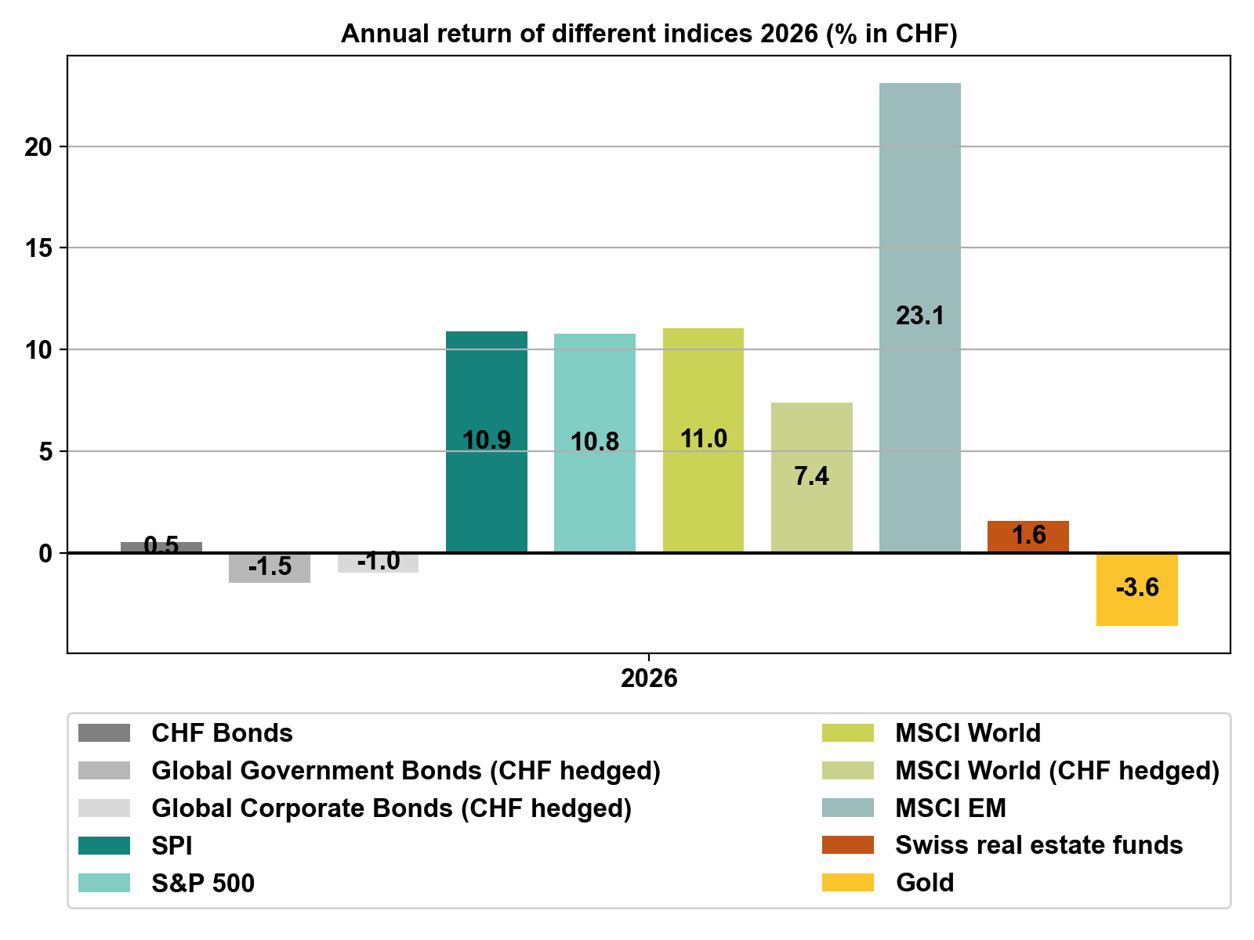

The positive earnings trend significantly supported share prices, while other asset classes such as bonds, real estate and even gold suffered from rising interest rates.

Despite geopolitical uncertainties, equities have delivered the highest returns amongst traditional asset classes year-to-date – with the exception of oil (see figure 4). This underscores its current relative attractiveness in an environment of volatile interest rates and solid corporate earnings.

Figure 4: Despite the geopolitical turmoil, equities have dominated the other asset classes (with the exception of oil) in terms of returns since the start of the year (data up to 02.07.2026). Source: Bloomberg, Swiss Life Wealth Managers.

Swiss Life’s new macroeconomic medium-term scenarios

What basic assumptions do all three scenarios share?

Transition to a multipolar world order

- The economic and military dominance of the US is declining over the long term. It is being replaced by an increasingly multipolar world order, in which China is an opposing pole. Russia is becoming part of the Chinese bloc, but continues to have influence in the former Soviet republics.

- Other developed economies, such as Japan, Canada, Australia and South Korea, remain closely linked to the US without forming an independent power bloc. Europe faces the challenge of strengthening its strategic autonomy and could establish itself as a pole in its own right in the medium term.

- The Global South – especially regions in Latin America, Africa, the Middle East and Asia – is gaining importance. It benefits from a wealth of raw materials and a growing working-age population and has the potential to become another economic focal point in the long term.

This geopolitical realignment influences supply chains, trade flows, technological cooperation, security alliances, and the role of the US dollar in the global financial system.

Demographic change and labour markets

With the exception of the Global South, demographic trends are leading to a structural shortage of labour and skilled workers in many economies. This increases wage pressure and favours more stable employment conditions, as companies are more keen to retain qualified staff even during economic downturns.

Structurally higher government spending

Investments in infrastructure, sustainable energy and defence are growing globally. These support growth but increase public debt.

Inflation and interest rates above pre-crisis levels

The combination of tight labour markets and rising government spending is leading to structurally higher inflation rates and long-term interest rates compared to the pre-Covid pandemic period.

Artificial intelligence as a growth driver

The expansion of AI infrastructure – especially data centres and energy supplies – is strengthening economic momentum, especially in the US and Asia. In the long term, the use of artificial intelligence offers significant potential for productivity and efficiency gains.

However, the scenarios differ in the speed and extent at which these productivity gains are realised.

Would you like to know what impact the current market situation might have on your personal situation?

Talk to our investment experts and arrange a free, non-binding initial consultation.

Baseline scenario: “what doesn’t kill the economy makes it stronger”

The past few years have demonstrated the remarkable resilience of the global economy. Despite repeated shocks – from the pandemic to geopolitical conflicts to the restructuring of the global economy – companies have been able to strengthen their adaptability through cost discipline and solid balance sheets. This financial flexibility forms an important basis for the further course of the economic cycle.

In the baseline scenario, we expect a gradual normalisation in the Middle East. Following the signing of the Memorandum of Understanding, we expect a gradual resumption of shipping through the Strait of Hormuz over the coming weeks and a peace agreement by the end of the year.

The political environment in the US is likely to change:

- we expect the government to lose control of Congress in the mid-term elections.

- At the same time, the fiscal momentum from the previous year will ease, while trade policy measures could gain in importance again.

- Against the backdrop of de-escalation in the Middle East, high budget deficits and rising public debt, US inflation is set to peak in the second half of 2026, then decline moderately, but remain above the central bank’s target until 2028.

Despite declining immigration, we expect economic growth in the range of potential, supported by ongoing investments in artificial intelligence and initial productivity gains.

In Europe, the picture remains mixed:

- in France, we expect government debt to rise further, irrespective of the outcome of the 2027 presidential elections.

- The EU is benefiting from the German fiscal programme in the short term, while the expiry of the “Next Generation EU” programme is having a dampening effect over the medium term. At the same time, increasing competitive pressure from China is likely to lead to increased protectionist measures.

Eurozone inflation is set to fall back to target levels in 2027. Supported by fiscal stimulus, we expect growth to be close to potential, but structurally significantly below that in the US.

In China, the real estate market is increasingly stabilising in major metropolises, thus easing the burden on the domestic economy. Growth remains strongly export-driven, especially in the area of advanced industrial goods. Protectionist measures in Western countries are only likely to slow this trend to a limited extent.

In terms of monetary policy, we expect falling inflation rates to create scope for the US Federal Reserve and the ECB to make interest rate cuts again from 2027. By contrast, the Swiss National Bank is likely to maintain a zero interest rate environment until 2028.

Despite potential monetary easing, we expect long-term government bond yields in the US and Eurozone to remain close to current levels due to rising debt and correspondingly higher risk premiums. In Switzerland, on the other hand, we anticipate a slight rise in long-term interest rates.

Corporate bond credit spreads are at historically low levels. In light of increased issuance activity to finance investments, we expect a moderate widening of spreads.

Equities remain the highest-yielding asset class in the base case scenario, supported by solid earnings developments. Elevated valuations combined with political risks and increasing discussions about potential overinvestment – especially in the AI space – are likely to lead to repeated increases in volatility.

For Switzerland, we expect the franc to appreciate further, to the extent that inflation at home remains below that abroad.

Swiss real estate continues to benefit from low interest rates and high demand, with slightly rising interest rates likely to dampen returns.

Commodities – with the exception of energy – are supported by high global investment activity.

First alternative scenario: “global recession”

In this scenario, the global economy slips into recession, triggered by either a demand or supply shock. Economic dynamics are different and the consequences for risky assets would be negative in both cases.

- Demand shock

A demand shock could arise, for example, from a loss of confidence in political leaders – especially in the US – or from disappointed expectations about the economic effects of artificial intelligence. As a result, private consumption and investment would decline significantly.

This would lead to a broad-based decline in economic growth with falling inflation at the same time. Central banks would react in this environment with interest rate cuts in order to stabilise demand.

- Supply shock

Alternatively, a recession could be triggered by an adverse supply shock, for example due to a breakdown in US-Iran negotiations and a re-escalation of the conflict in the Middle East. A shortage in the oil supply would push up energy prices significantly and weigh on consumption and economic activity.

In this case, real growth would decline, while inflation would initially rise and only decline with a lag. Central banks would face a trade-off: in the short term, higher interest rates would be needed to combat inflation, which would further aggravate the economic slowdown before an easing of monetary policy would be possible at a later date.

Impact on financial markets

Regardless of the trigger, risky asset classes such as equities and corporate bonds would record significant losses in a recession environment, driven by falling earnings expectations and rising risk aversion.

The performance of other asset classes would be more nuanced:

- Government bonds would perform positively in the event of a demand shock thanks to falling interest rates, while in the event of a supply shock they may initially suffer from rising inflation expectations.

- Listed real estate is sensitive to interest rate developments and would therefore perform differently depending on the scenario.

- Commodities would benefit from rising prices in the short term during a supply shock, but come under significant pressure in the event of a demand shock.

Second alternative scenario: “accelerated economic upturn”

In this scenario, the global economy would perform significantly more dynamically than in the baseline scenario. This would be driven by either faster declining energy prices – for example, following an easing of sanctions on Russia or Iran – or a stronger-than-expected productivity increase due to the widespread use of artificial intelligence.

Both developments would initially have a disinflationary effect: Falling energy prices reduce production costs, while productivity gains increase growth without directly generating price pressure. As a result, the central banks could initially maintain a comparatively expansionary monetary policy despite the strong economy, high investment activity and robust consumer demand.

However, inflationary trends are increasing over the forecast horizon. The combination of persistently strong demand, high capacity utilisation and expansionary fiscal policy is leading the central banks to gradually shift to a tighter monetary policy.

Impact on financial markets

Risky asset classes in particular would benefit in this environment:

- Equities would generate above-average returns driven by strong earnings growth.

- Real estate would also perform positively due to favourable financing conditions and high demand.

- Commodities would benefit from high global investment and manufacturing activity, with energy prices tending to remain under pressure depending on the triggers.

- Corporate bonds would perform solidly, supported by low credit spreads.

However, with the later onset of monetary policy tightening, interest-rate-sensitive asset classes such as government bonds and, to some extent, real estate would come under increasing pressure.

What should investors do?

Our base case scenario assumes a solid macroeconomic environment. Investments in infrastructure, artificial intelligence, sustainable energy and defence as well as a robust labour market and stable private consumption are supporting growth.

Companies have demonstrated impressively their resilience to crises in recent years. Solid balance sheets, cost discipline and high adaptability will enable them to continue reacting to a challenging environment going forward. Investors benefit from this through rising corporate profits, which are reflected in both price gains and dividends.

Bonds abroad are under pressure due to rising government debt. Swiss bonds remain only to a limited extent given the low interest rate environment.

Against this backdrop, we continue to favour real assets such as equities, real estate and selected commodities, which benefit from elevated levels of global investment activity.

At the same time, the recession scenario makes it clear that conscious risk diversification remains key.

Important principle for investors:

Do not be unsettled by short-term volatility. A more defensive positioning over the long term than that which corresponds to your risk profile is not warranted in the baseline scenario. What is key is a long-term investment strategy that remains viable even in difficult market phases and offers the necessary orientation and stability, especially in uncertain times.

Dr. Peter Kaste

Chief Investment Officer (CIO), Swiss Life Wealth Management Ltd

Peter Kaste is the Chief Investment Officer at Swiss Life Wealth Management Ltd. He holds a doctorate in physics and is a CFA charter holder, a member of the Swiss CFA Society, and a lecturer at the Lucerne School of Business. Following his doctorate, Peter Kaste worked as a researcher for several years at École Polytechnique (Paris) and ETH Zurich. He has worked in asset management since 2006. Between 2008 and 2023, he established and headed the Quantitative Research Team at Swiss Life Asset Managers. He has been Chief Investment Officer heading up Investment Management at Swiss Life Wealth Managers since 2024.

Note: the information provided is for information purposes only and is without guarantee and liability. It does not constitute an offer, investment advice or a recommendation to acquire or sell financial instruments or to conclude any other legal transactions. This article contains forward-looking statements, which express our assessment and expectations at a given point in time. However, various risks, uncertainties and other influencing factors can cause the actual developments and results to differ significantly from our expectations. Past performance is no indicator of current or future developments and results. Investments in financial products involve various risks, including the potential loss of the invested capital.