The Swiss economy and the domestic stock market have coped well with the customs shock of 1st August so far. One key reason for this is that the most important export goods have so far been exempt from customs duties. At the same time, the US Federal Reserve is coming under increasing political pressure, which is weighing on the US dollar and could cause US inflation expectations to rise. On the financial markets, the Fed's first interest rate cut this year brought relief – prices are continuing their rally.

Key points at a glance

On 1st August, Switzerland was surprised by the imposition of high US import tariffs: the US government is levying duties of up to 39% on certain goods from Switzerland. What is particularly painful for Swiss industry is that important competitors have been subject to significantly lower tariffs. However, the effect on the Swiss economy and the stock market has been minimal so far, as pharmaceutical products and gold, the two most important export goods, have been exempt from tariffs. The financial markets are currently more concerned about the US government's increasing political influence on the US Federal Reserve (Fed). By filling vacancies on the Federal Reserve Board with its supporters and attempting to dismiss a governor of this board, the government is seeking to exert direct influence on US monetary policy. However, the political independence of the central bank is crucial to keeping inflation expectations stable and not jeopardising confidence in the US dollar. The Fed itself is currently in a quandary: while the goal of price stability would continue to require a restrictive monetary policy, a cooling US labour market suggests interest rate cuts. With the first interest rate cut of this year on 17th September, the Fed gave priority to the labour market. Investors reacted with relief and now expect further interest rate cuts. Falling key interest rates, combined with a still robust economy and rising corporate profits, are giving further momentum to the stock market rally that has been ongoing since April. Details of our expert assessment can be found below.

What does the customs shock of 1st August mean for Switzerland?

On 1st August, the Swiss not only celebrated their national holiday, they were also surprised by the imposition of US import duties of 39% on Swiss goods. What is particularly painful is that only Laos, Myanmar and Syria have been hit with even higher tariffs of 40% to 41%, while all major competitors have been subject to significantly lower tariffs of 10% to 20%. In addition to the strong Swiss franc, the higher import tariffs are now also reducing the competitiveness of Swiss companies in the US market.

However, the import tariffs imposed on 1st August are subject to the same exemptions as those imposed on 2 April. The two most important Swiss export goods remain exempt from the duties:

- pharmaceutical products

- gold

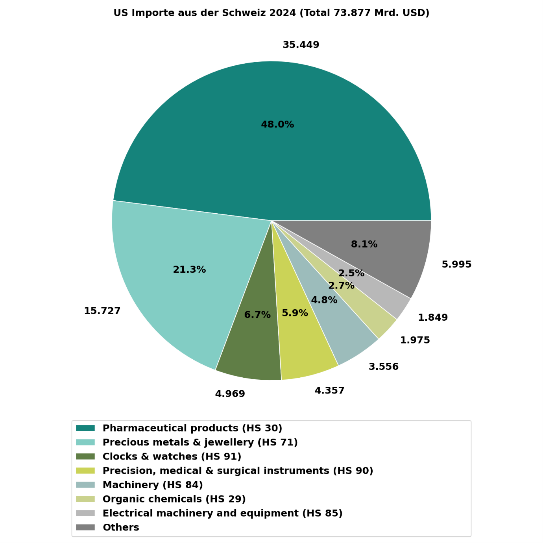

As Figure 1 shows, Switzerland exported goods worth a total of USD 73,877 billion to the US in 2024. Of this, pharmaceutical products accounted for approximately 48% with a value of USD 35,449 billion. Precious metals and jewellery are the second most important product group, accounting for USD 15,727 billion or 21.3%, with gold making up the majority of this product group.

Figure 1: US imports from Switzerland are dominated by pharmaceutical products and precious metals. Watches, precision instruments and machinery are other important product groups that are affected by the tariffs imposed on 1 August. Sources: United Nations Comtrade Database, Swiss Life Wealth Managers

Swiss stock market successful despite tariff shock

The exemption of these two important export goods is likely to be a key reason why the Swiss stock market hardly reacted to the tariff shock. On the contrary: in August, the Swiss stock market (SPI Index) was one of the world's best-performing stock markets, with a return of 2.31% measured in Swiss francs.

There are other explanations as well:

- Firstly, there is hope that Switzerland will be able to persuade the US President to reduce tariffs by making further concessions.

- Secondly, it is legally unclear whether US President Trump is even entitled to impose tariffs of this magnitude under the International Emergency Economic Powers Act (IEEPA), which he is invoking. Two US courts have already ruled against this, and the US Supreme Court will decide on this issue in October.

- Thirdly, a distinction must be made between the economy and the stock market. A decline in exports from Switzerland reduces GDP, puts pressure on the Swiss labour market and reduces government tax revenues. However, for globally active Swiss companies that have production sites abroad, can relocate production abroad and serve the US market from there, the damage is manageable. A stock market dominated by globally active companies may well perform better than the local economy in the event of a tariff dispute. However, manufacturers for whom ‘Swiss Made’ is an important selling point suffer particularly badly from tariffs. This includes the watch industry, for example.

Swiss Life economists have revised their GDP growth forecast for Switzerland downwards for the coming quarters. The longer the customs tariff gap with competitors remains, the greater the impact that shifting production capacity abroad is likely to have on Swiss economic growth.

Quo vadis, Switzerland as a pharmaceutical location?

The threat of US import duties on pharmaceutical products hangs over the Swiss economy like the sword of Damocles. On the night of 25th to 26th September, the US President announced on social media that import duties of 100% would apply to pharmaceutical products from October onwards – unless the companies concerned build new production facilities in the US. No details of this announcement or official executive order have been released as yet.

The share prices of the two pharmaceutical heavyweights Novartis and Roche reacted moderately to this announcement with daily returns of +0.41% (Novartis) and -0.59% (Roche). Both have production capacities in the US and have already significantly increased their inventories there in anticipation of the introduction of tariffs. This gives them some time to analyse the new situation.

Would you like to know what impact the current market situation might have on your personal situation?

Talk to our investment experts and arrange a free, non-binding initial consultation.

Political pressure and rising unemployment in the US

The US Federal Reserve (Fed) currently finds itself in a challenging position. It has a dual mandate, under which it is required not only to ensure monetary stability but also to promote full employment.

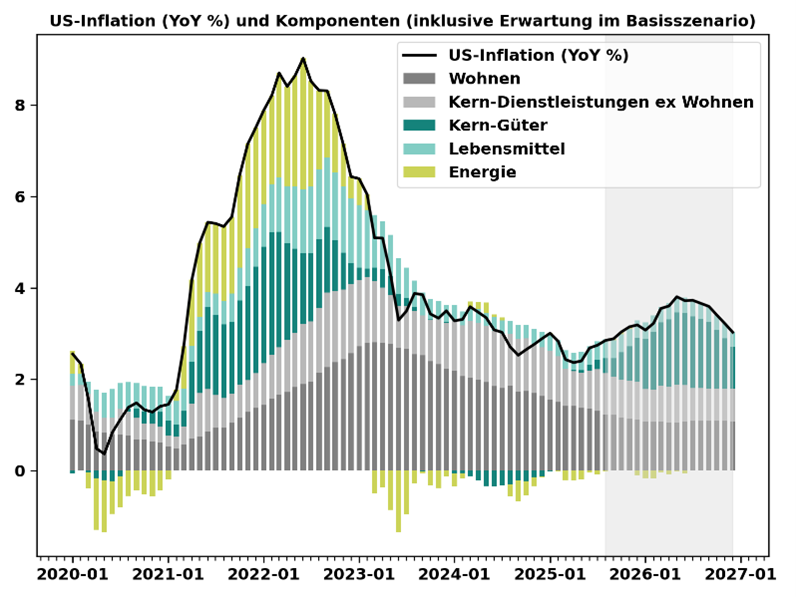

At the end of August, US inflation stood at 2.9%, above the Fed's target, and rising. This trend is being reinforced by the US government's policies: new tariffs, an extremely expansionary fiscal policy and a restrictive immigration policy are driving inflation further (see Figure 2).

Figure 2: US inflation is above the Fed's target level and has risen recently. US import tariffs are likely to cause a further rise in inflation, particularly in the core goods sector. The grey area shows the expected inflation trend in Swiss Life's base scenario. Sources: Swiss Life Asset Managers, Swiss Life Wealth Managers

Job losses in the US – prominent dismissal at the BLS

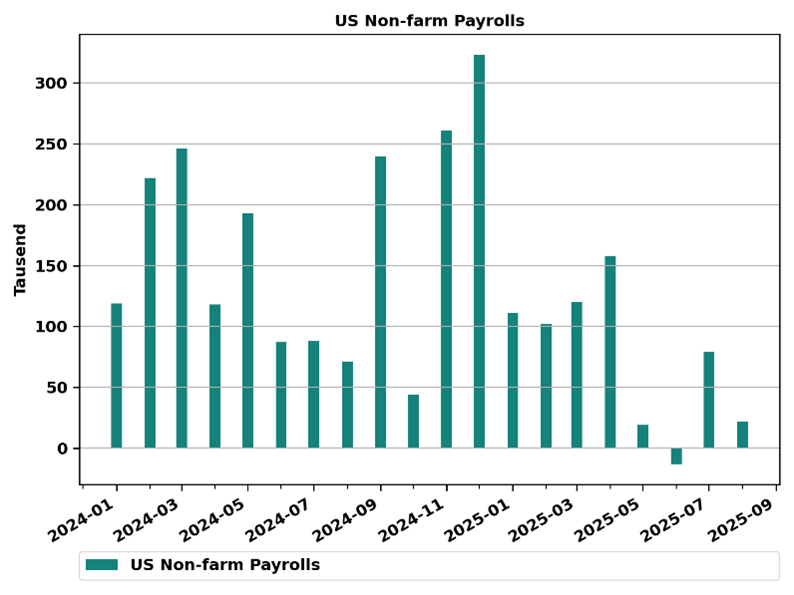

On 1st August, the US Bureau of Labour Statistics (BLS) published its monthly labour market report for July. In it, the number of jobs (excluding agriculture) for the previous two months was revised significantly downwards:

- by 125,000 jobs for May

- by 133,000 jobs for June

In the report of 5th September for the month of August, the change in the number of jobs for June had to be revised downwards again by 27,000 jobs to –13,000 jobs. This was the first decline in non-agricultural jobs since December 2020 (see Figure 3).

A cooling of the US labour market had been expected as a result of erratic US trade policy. Nevertheless, US President Trump dismissed the head of the Bureau of Labor Statistics, Erika McEntarfer, on the unfounded accusation that she had manipulated the labour market data to his disadvantage.

Figure 3: The revised monthly labour market reports from the Bureau of Labour Statistics (BLS) point to a slowdown in the US labour market. In June of this year, the number of jobs outside agriculture fell for the first time since December 2020. Sources: Bureau of Labour Statistics (BLS), Bloomberg, Swiss Life Wealth Managers

These labour market reports presented the Fed with a dilemma due to its dual mandate: should it maintain a restrictive monetary policy in order to reduce inflation, or should it lower interest rates to support the labour market?

On 17th September, the Fed opted for the latter and cut its key interest rate (the upper limit of the Fed Fund Rate target range) from 4.5% to 4.25% for the first time this year.

Political pressure on the Fed is mounting

However, the US government still considers the central bank's monetary policy to be too restrictive. It would like to see lower interest rates, as this would stimulate the economy and at the same time make it cheaper to finance the high budget deficit.

Fed Chairman Jerome Powell in particular has long been the target of harsh verbal attacks from the US President. Although these attacks are distasteful, they have not influenced the Fed's monetary policy so far. Far more worrying are the US government's attempts to replace the Federal Reserve System's governing body – the Board of Governors – with its own supporters.

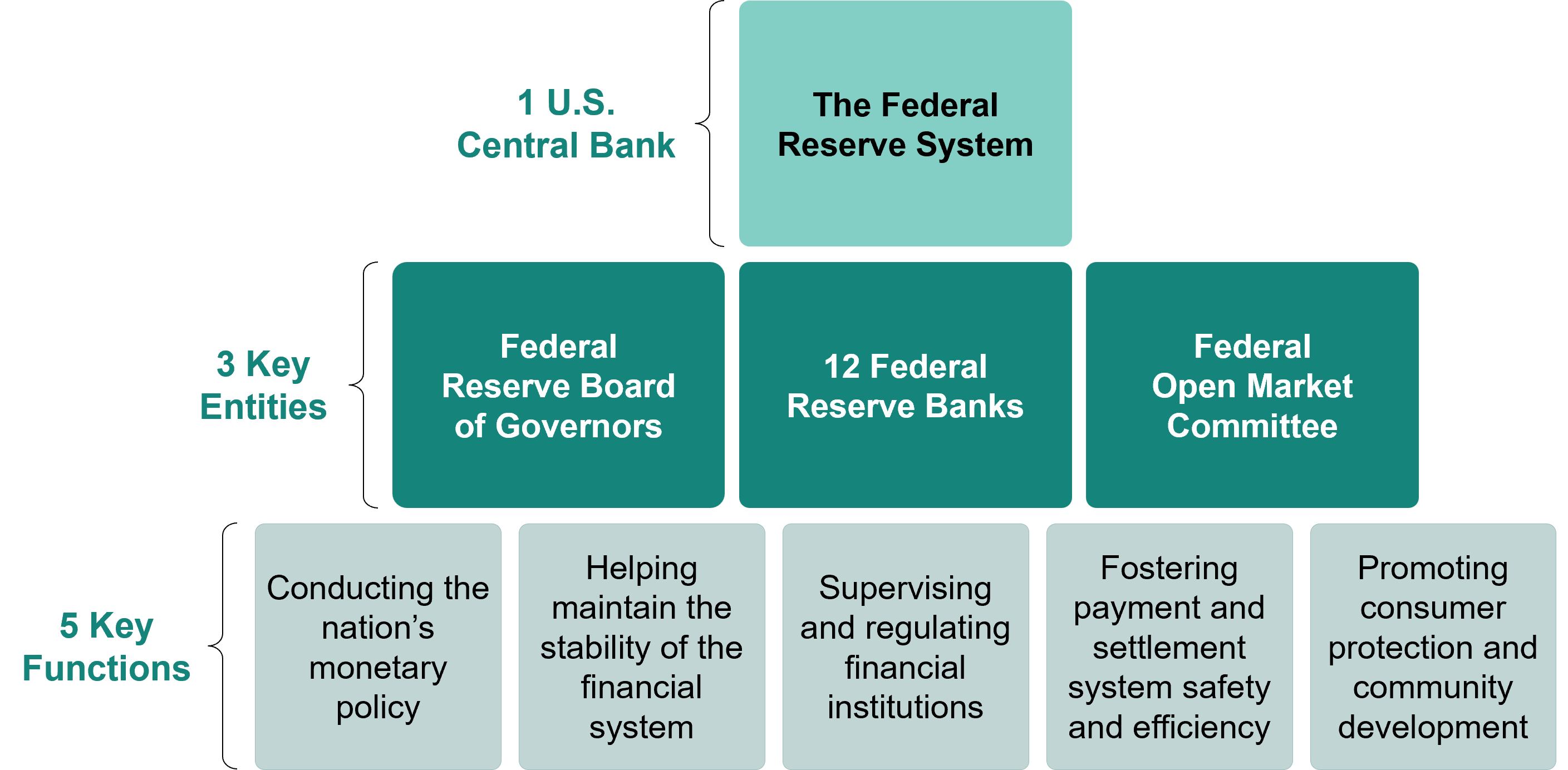

Figure 4 shows the structure of the US Federal Reserve System.

Figure 4: The structure of the US central bank consists of three main elements: the Federal Reserve Board of Governors as the governing body, the twelve regional Federal Reserve Banks as operational units, and the Federal Open Market Committee, which makes monetary policy decisions. Sources: Federal Reserve, Swiss Life Wealth Managers

How the Fed is structured

The Federal Reserve Board consists of seven governors, each appointed for a 14-year term. They are nominated by the US President, must be confirmed by the Senate and can only be dismissed by the US President for good cause.

These rules ensure the political independence of the board and the central bank. The Chair and Vice Chair of the Federal Reserve Board are nominated by the US President from among the seven governors for a term of four years and confirmed by the Senate.

The Board oversees the Federal Reserve System and, among other things, confirms the presidents and vice presidents of the twelve regional Federal Reserve Banks for terms of five years.

The Federal Open Market Committee, which makes monetary policy decisions, consists of a total of twelve members with voting rights:

- all seven governors of the Federal Reserve Board,

- the president of the regional Federal Reserve Bank of New York,

- and four other presidents of the remaining regional Federal Reserve Banks on a rolling annual basis.

The presidents of the other seven regional Federal Reserve Banks may participate in the discussions of the Federal Open Market Committee, but do not have voting rights.

Risks of politically motivated monetary policy

A politically motivated, overly expansionary monetary policy can lead to rising inflation and low or even negative real interest rates. This allows debtors, including the government, to borrow cheaply and can stimulate demand in the short term. Those who save and/or invest in bonds suffer from such monetary policy, as their purchasing power declines due to inflation. In this case, the currency depreciates. Even if a central bank keeps short-term interest rates artificially low, long-term interest rates on the financial market are determined by supply and demand and should tend to rise. To prevent this, the central bank could intervene, for example by:

- buying long-term government bonds itself,

- forcing financial institutions to buy more long-term government bonds through financial market regulation,

- or returning to a more restrictive monetary policy.

The financial markets will be watching closely to see how far the Fed's attempts at political influence will go and whether the US central bank will continue to pursue both objectives of its mandate.

The governors can influence US monetary policy both through their own voting behaviour in the Federal Open Market Committee and through the confirmation of the presidents of the regional Federal Reserve Banks.

Financial markets continue their rally

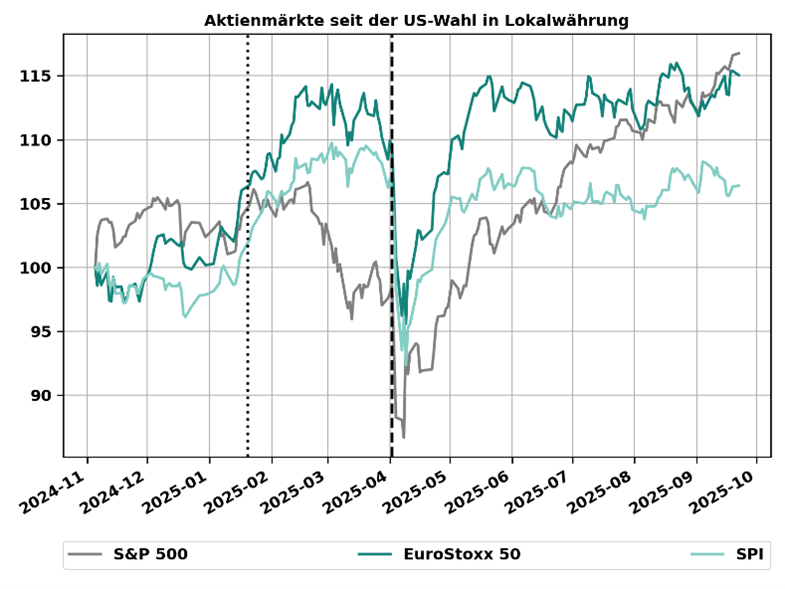

The stock markets have been rallying since the US President announced the introduction of reciprocal.

Figure 5: Stock markets have been rallying since 9th April. In local currency terms, the US market in particular has caught up strongly. Sources: Bloomberg, Swiss Life Wealth Managers

While the rally was initially driven by hopes of a negotiated solution to the tariff dispute, it was sustained by declining uncertainty following the first agreements. A strong reporting period for second-quarter corporate results fuelled confidence that corporate profits would grow more strongly than expected, which benefited the US market in particular.

So far, the Fed has enjoyed the confidence of the financial markets. The first interest rate cut this year and the prospect of further cuts were therefore well received: falling financing costs are boosting the profits of American companies, while a falling US dollar is providing additional support.

USD interest rates fluctuate with changing expectations of Fed interest rate cuts. Short-term USD bonds should initially benefit from falling interest rates, while concerns about rising inflation will eventually prevail for long-term USD bonds.

Ten-year interest rates on Swiss government bonds have fallen to around 0.2% as a result of the gloomy economic outlook following the tariff shock and are not very attractive to investors.

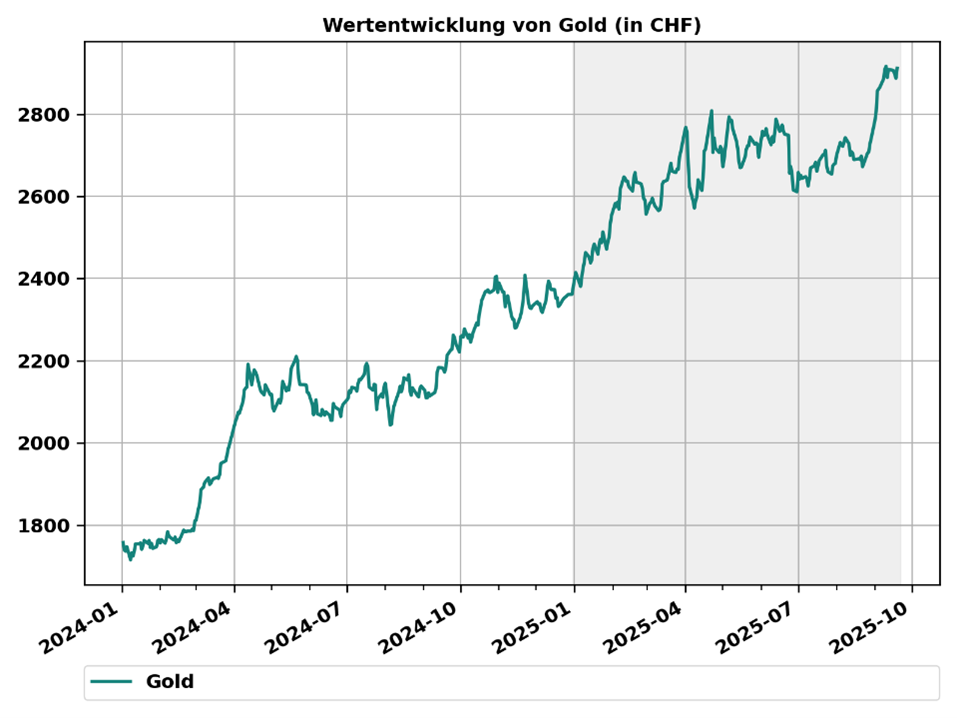

Figure 6: Gold has continued its rally of the last two years since the summer. The rise in the price of gold is not solely a consequence of the weak US dollar, as demonstrated by its performance in Swiss francs. Sources: Bloomberg, Swiss Life Wealth Managers

How should investors respond?

Many investors will be wondering whether now is the right time to take investment risks. To be honest, however, my concern in the medium term is more about very defensive investors who have invested their money in savings accounts or bonds at low interest rates, especially low real interest rates.

Those who have the investment horizon, risk capacity and risk appetite to invest with a more dynamic profile will benefit from significantly higher return opportunities.

Especially in uncertain times, it is crucial to remain calm and focus on the long-term strategy.

Dr. Peter Kaste

Chief Investment Officer (CIO), Swiss Life Wealth Management Ltd

Peter Kaste is the Chief Investment Officer at Swiss Life Wealth Management Ltd. He holds a doctorate in physics and is a CFA charterholder, a member of the Swiss CFA Society, and a lecturer at the Lucerne School of Business. Following his doctorate, Peter Kaste worked as a researcher for several years at École Polytechnique (Paris) and ETH Zurich. He has worked in asset management since 2006. Between 2008 and 2023, he established and headed the Quantitative Research Team at Swiss Life Asset Managers. He has been Chief Investment Officer heading up Investment Management at Swiss Life Wealth Managers since 2024.

Note: the information provided is for information purposes only and is without guarantee and liability. It does not constitute an offer, investment advice or a recommendation to acquire or sell financial instruments or to conclude any other legal transactions. This article contains forward-looking statements,which express our assessment and expectations at a given point in time. However, various risks, uncertainties and other influencing factors can cause the actual developments and results to differ significantly from our expectations. Past performance is no indicator of current or future developments and results. Investments in financial products involve various risks, including the potential loss of the invested capital.